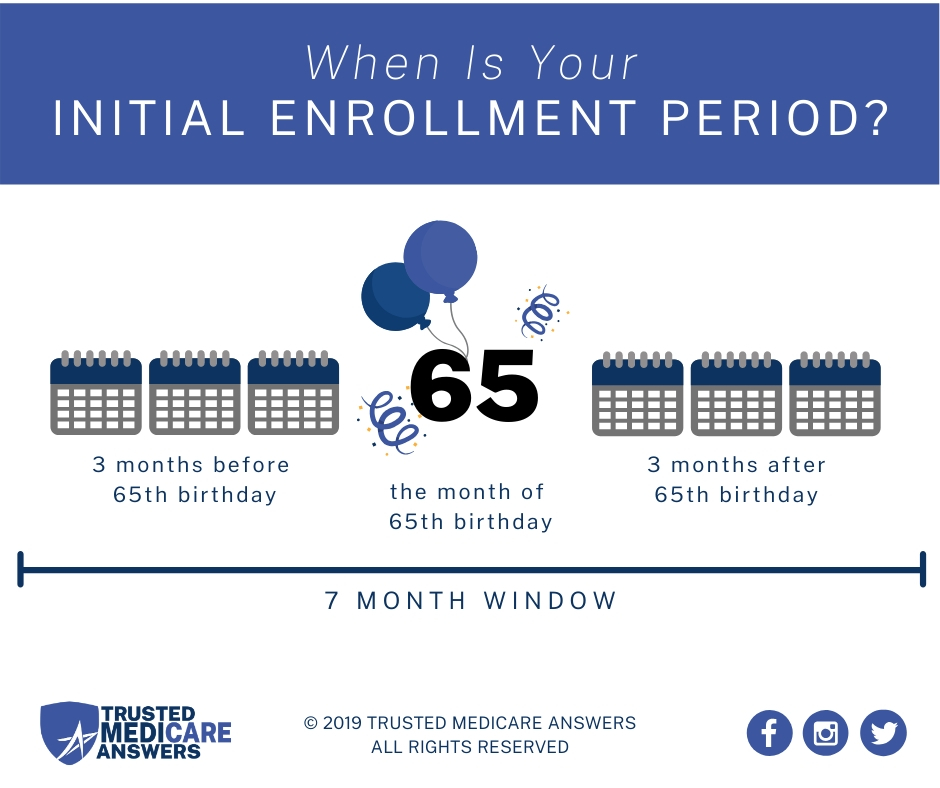

The age of retirement seems to be delayed longer and longer for most Americans, leaving many confused about when to enroll in Medicare. While the standard is to enroll within three months from your 65th birthday, many people assume they do not have to if they will still be receiving health insurance from their employer. This misconception could lead to penalties and fees that could have otherwise been avoided. Let’s break down the scenarios for enrollment to ensure that you are never left uncovered.

Generally, if you are working for an employer with more than 20 employees, your group insurance should continue to cover you. While this may be comforting to many, you should still consider enrolling in Medicare Part A. If you have worked for at least 10 years in the US, then you will qualify for Part A without premiums. Not only is this a no-cost option, but it also will give you secondary coverage to potentially pick up the costs that group insurance did not. You will also have the opportunity to delay Part B, however, this option should be made based on your current group insurance to analyze the costs and coverage included. What may be a good choice for someone else may not be preferable for you. It may be in your best interest to consult an independent insurance agent specializing in Medicare to help navigate your alternatives.

If your company happens to be smaller, with less than 20 people, then you are required to sign up for Medicare Part A and B when eligible, rather than waiting. The consequences of waiting are, unfortunately, financial penalties and possible lapse in coverage. For Part A, your monthly premiums increase 10% and will last for twice the amount of years you should have been enrolled but weren’t. The repercussions for Part B late enrollment are more significant. You may be subject to 10% premium increases for every year you did not enroll, lasting for the entirety of your Part B. For example, if you waited two years to enroll you may have to pay 20% for your monthly premiums for as long as you have part B. Some people may be eligible for a Special Enrollment Periods (SEP) in which they can enroll for Part A and B without late-enrollment fees. For example, being covered by your employer through group insurance qualifies you for an SEP, which is why you are able to delay.

Make sure you know when to sign up for Medicare if you are still working at 65 to prevent unnecessary costs or gaps in coverage. If your situation is more complicated, or you just want more questions answered, consider a free consultation with an independent insurance agent specializing in Medicare. It’s free and there’s no obligation, but you will likely find the answers you need.